How banks + SaaS = small business online boom

Banks are fast becoming technology companies that integrate finance with other offerings – they were partly forced to do so when new challenger banks arrived on the scene, but now there’s an opportunity for both traditional banks and challenger banks to go a step further.

McKinsey said as much in their recent report, in which they recommended that banks seek to become a one-stop shop for small business enablement tools.

Several McKinsey partners expanded on the report in an interview. “Since [banks] already offer mortgages, why not provide the end-to-end journeys of buying and owning the home?” said Miklós Gábor Dietz, Senior Partner at McKinsey. “Banks are also well positioned to orchestrate the small-business ecosystem, combining their existing banking relationships with administrative, technology, HR, even software services.”

Banks have the power to stitch together tools – their own and those of partners – becoming even more foundational to small businesses in the process. Banking, accounting and transacting all tie back into a bank’s core offering, and if banks can take customers from their first business bank account to their first transaction, they could become the next base camp for selling online.

In our last article on the subject, we explored how banks can use software ecosystems to win small businesses. We saw that three options were available to them: Be a provider, a builder, or an orchestrator.

In this article, we’re going to focus on how banks can orchestrate a digital experience for their small business customers – and how they can get the partnership and support they need.

1. Outline your vision for the experience

If you’re orchestrating a digital experience for your small business customers, your vision is likely bigger than becoming a vendor. You’re looking to do more than offer a buffet of small business products, you’re offering an effortless journey from where they are now to where they want to be i.e. their entire business is up and running.

Paul Simon, a former business growth specialist at ActionCOACH, spent 30

years in banking and finance and contributed to our 2022 Small Business report. “We know that small businesses roughly have about 20 minutes on a Sunday afternoon to think about running their business,” says Paul. “The rest of the time they’re working in it.”

For such busy customers, ease will be the main selling point – so you’re going to want to make the UX between the various components as tightly integrated as possible. You’ll want them sharing data so that the user doesn’t need to use different logins or repeatedly input the same information, for instance.

Fiona Roach, the CEO of Pollinate, wrote as much in her Forbes article on How Banks Can Beat Fintechs.

“What’s the first data you input when signing up with a new bank, or any other product or service?” she wrote. “Chances are it will be simple biographical details such as name, address, telephone number and similar. What can serve to undermine customer experience is the need to input this data repeatedly.”

“Banks that can successfully pull together different data inputs—their own and those from third parties—to create really integrated and seamless front-end experiences can offer customers the feel of a fintech, with the security and products of a bank.”

Along with data integration, the user interface also needs to feel integrated across all touch points. If all the components look different and behave differently, it’s going to be a jarring experience for your small business customers.

2. Define the components of your vision

It’s also worth defining exactly what your experience should and shouldn’t include – and where you can and can’t afford to compromise.

In an ideal scenario, your bank would offer everything a small business could possibly want in a totally branded experience – but your time is limited and the tighter your focus, the more likely you’ll be able to create an ecosystem of high value to customers and your bottom line.

There’s no point in banks selling SaaS for the sake of it, therefore. And we’d suggest, from our own conversations with banks and payment providers, that one of the first priorities should be to close the transacting loop. If banks can do this they stand to benefit not only in terms of customer retention but also in terms of transaction volume and fees.

To close the transaction loop, banks will primarily need to offer: a bank account, accounting tools, a platform where transactions can take place, and payment gateways that bring funds in.

You can be tactical about what you build, what white label tools you use, and where you can afford to work publicly with partners. For instance you might offer payment gateways and e-commerce stores to your customers as a branded experience, but for accounting tools you may prefer to publicly partner with an established accounting application – like Xero or Quickbooks – since you know these brands already hold trust with your customers.

3. Partner with SaaS companies that suit your vision

The next element you’ll need to lock down is the willingness of the partners you choose. Not just the willingness to be a part of an integration, but the willingness to customise their software and really work with you to get the integration tight with the other parties involved. A leading digital ecosystem is going to require more work than plugging in off-the-shelf software.

The tighter you can get the integration, the faster and easier your customers will be able to receive their first online payment – and the faster they’ll see the value of what they’ve just bought into.

Our CEO Simon Best spoke of this principle in our micro business report: “It sounds obvious but you need to make the path to that point of value really smooth, and you need to ask how you can make the path shorter, how can you make it as fast as it can be.”

So you want partners that are willing to make this happen. But naturally it’s not enough to have partners with enthusiasm, they’ll also need the technical capabilities to support your vision.

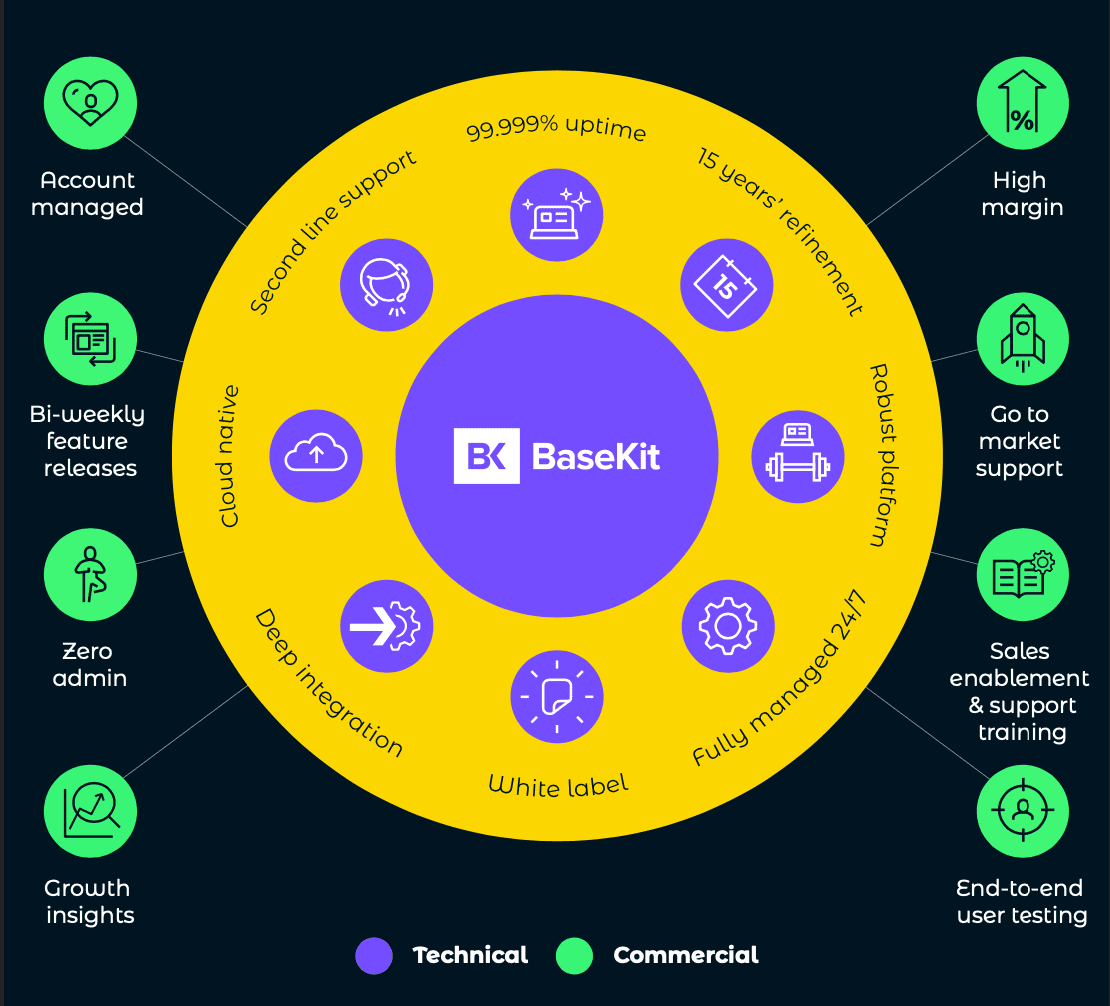

Qualities that you’ll want in a good integration partner include:

- Market-proven software

- Record uptime

- 24/7 management

- Second line support

- End-to-end user testing

- Go to market support

- Regular updates and feature releases

- Growth insights

What makes a successful partnership?

Also, if there’s a chance you’ll be onboarding 5,000 new customers a month in multiple languages, you’ll need partner software that’s ready for hyper localisation and scale.

4. Follow through on your vision in your market positioning

If you’re able to do all of the above, you’ll be offering an integrated experience that isn’t yet found anywhere on the small business banking market – although there are plenty of fragmented examples out in the wild

You’ll want to do it justice in your positioning and marketing. Having partnered with plenty of companies to sell our own white label software, we’ve seen prime examples of what to do and what not to do. Those that position themselves like a marketplace, and treat their vendors’ products like a catalogue of stock, tend to be the least effective.

Our partners who have seen the most success are those that have been able to package an integrated offering that promises to deliver a single outcome to their customers – this might be “everything you need to run an online store.” And your targeted advertising can get even more specific – perhaps “everything you need to turn your hobby into an online business”.

For more ideas on how banks can partner with SaaS platforms to get small businesses selling online, see our articles on why banks will be the next base camp for selling online and the first 30 days – how banks will win small business customers for a lifetime

We’re on a mission for tech democracy for small businesses. Request a demo of our software, or get in touch to discuss what a BaseKit partnership could look like.